Prepare your business for sale to maximise the value

About the Author: Ashley Thomson

We’ve worked with a number of business owners who came to us seeking guidance on navigating the sale of their small business.

A few had received unexpected (and somewhat underwhelming) offers from potential buyers. They realised that they needed guidance on how to improve the ‘kerbside appeal’ of their businesses to attract the best price.

Some simply felt they’d taken their business as far as they could on their own. They were thinking about selling to someone who could take what they’d started to the next level.

A couple had simply lost passion for their business or felt stuck. Selling just seemed like their only option to exit the business.

Every business plan needs a good exit strategy

In our previous blog series about succession planning in your family business, we touched on selling as a potential exit strategy.

The key takeaway from that series was that regardless of which strategy you choose, exiting your business should never be done on impulse. A successful transition of ownership takes significant planning and preparation.

Six ways you can prepare your small business for sale

We mentor our coaching clients to follow this plan for preparing for sale.

(Fair warning: there have been some unexpected outcomes… but we’ll come back to that.)

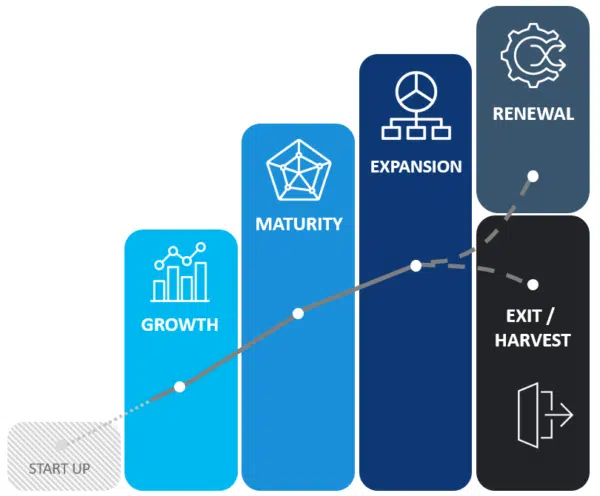

Time it right: the lifecycle of a business

There are four stages in the business lifecycle:

Startup – Growth – Maturity – Decline/Renewal (or Harvest/Exit)

The ‘sweet spot’ for selling is often said to be somewhere between the end of the growth stage and the beginning of the maturity stage.

During the startup stage, any value the business has is tied up in its potential. The level of risk is most often too high for most buyers.

In the stage of decline and/or renewal, the business sits at a crossroads. A much greater level of investment, repositioning and change within the business may be required to entice prospective buyers to offer their best price.

Get yourself in the right headspace

In a perfect world, you’d have been thinking about selling your business since the day you started it. But realistically, not many small business owners think this way.

Most have an emotional attachment to their business; they dreamed of creating a certain lifestyle and an ongoing source of financial security for themselves and/or their family.

Look, you may see your business through rose-coloured glasses but a buyer will be making a business decision, not an emotional one. To make the necessary changes that will attract the big bucks, you’ll need to develop some objectivity.

Which leads us to…

Change your lens and put on some customer-coloured glasses

This is the key to really whipping your business into the best possible shape. To increase buyer appeal, you will need to:

- Demonstrate an exemplary financial record

No one wants a financial ‘fixer-upper’. At the very least you’ll need to prove that the business enjoys a stable cashflow. Make the investment and get the best financial advice you can afford – you’ll see the benefits come sale time. - Remove the risk

Aim to create stability by locking down informal agreements, long-term real estate deals and generally tying up any other financial loose-ends. If your revenue depends on just one or two big clients, you may need to work on diversifying your income stream. The ultimate goal is to make a potential buyer’s decision to purchase as easy as possible. - Develop an independent, top performing team

Make sure all your staff have completed any necessary training and accreditation and support them to fill any gaps in their skills and experience. Make sure that everyone in the business can perform their role in your absence. Being able to step away from the business is an attractive prospect for buyers. It also helps protect your team’s future employment with the business (since they are less ‘dispensable’). - Create and document failsafe processes

Processes and information are of no use to a prospective buyer if they’re all stored in your brain. They’ll want to know that your business is run using effective management systems. Make sure you can demonstrate the you regularly run up-to-date reports on accounting, performance and customers and act upon the insights gained. - Show great potential

‘Room to grow’ is an essential element of attracting a top offer for your business. Buyers will want to know they can expect a good return on investment (ROI) and growth is a big part of that.

Spy on successful sellers in your industry

Just as with selling your home, keeping track of what comparable businesses sell for can be a good way to get a handle on the market and understand what variables affect a business’ perceived value. You’ll also get a feel for how ‘in-demand’ a business in your industry may (or may not) be.

Know your worth: 3 methods to value your business

There are a few ways you can get an idea of the value of your business. None are an exact science – there are always other factors involved – but even a general figure can help you make key decisions about what next steps you wish to take. Here are three commons methods for how to value your business for sale.

Method 1. Value of assets

This method quite simply gives you the value of the business based on its current assets (cash, stock, equipment, intellectual property etc), minus all liabilities (debts, payments due etc).NB: This isn’t a very reliable method for valuing a successful business, since it doesn’t take goodwill into account. ‘Goodwill’ refers to the less tangible value a business has. Factors such as brand equity, reputation, business history, location etc can mean that a business’ true value is much greater than a ‘value of assets’ calculation suggests.

Method 2. Return on Investment

This common valuation method uses the expected return on investment (ROI) to calculate the value of your business:

- Work out your average net profit (look at net profit for the past few years to give you some idea of how your business typically performs)

- Calculate the expected return on investment (expressed as a %) – ROI = expected profit/cost x 100

- Calculate your selling price – Selling price = (average net profit/ROI%) x 100

Method 3. Earnings multiple

This method takes your earnings before interest and tax (EBIT) and multiplies it by a ‘business earnings multiple’ to calculate your business’ value.

Note: Since the ‘multiple’ varies according to industry and business type, as well as the level of risk and growth potential of your business, we advise our clients to seek professional advice from a business valuer for the most accurate figure. You can find other business valuation methods at Investopedia.

Keep an open mind about potential buyers

It’s common to imagine that whoever buys your business will bear more than a passing resemblance to yourself.

You may be surprised, therefore, to see a competitor or larger company come sniffing around hoping to buy up the competition. You may even receive an out of the blue offer from an unexpected source – an existing employee, for example.

The type of buyer your business attracts will have a direct impact on the kinds of offers you receive. To achieve the highest possible sale price, we mentor any of our coaching clients looking to sell to stay open to all possibilities.

Of course… there may be one potential ‘buyer’ you haven’t considered

More often than you’d think, having made all the preparations for sale, some of those clients who had been so keen to hand over their business to the highest bidder, never quite get around to putting up that ‘for sale’ sign.

Anyone who has prepared their home for sale will understand why. Now that you’ve fixed up all the niggling problems and given everything a proverbial ‘fresh coat of paint’, you’re seeing your business with new eyes.

If, at the end of this process, you’ve done such a great job of preparing your business for sale that you’ve sold yourself on keeping it, that’s still a great outcome. Now you can just enjoy it!

A ‘seller’s mentality’ is best for your business

It’s important to build and grow your business in a way that ensures it would fetch the highest price possible – even if you have no intention of ever selling. Why? It forces you to adopt best practices. By optimising your business ‘for sale’ you unlock all the potential. Then, by choosing to stay in it, you get to be the lucky one who reaps those rewards.

If you’re considering the future of your business call us on 03 9813 8777 or click here for more information our business coaching services to sell a business.